Why the 4% Rule is a Lie: Advanced Withdrawal Strategies for Financial Independence

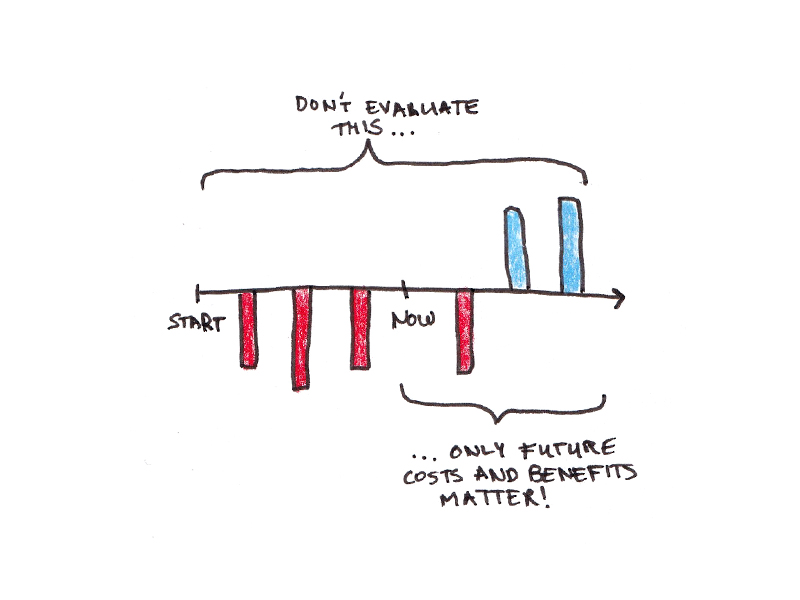

For decades, the 4% rule has been the gold standard for retirement withdrawals. The idea is simple: withdraw 4% of your portfolio in the first year of retirement, adjust for inflation each year, and your money should last 30 years or more.

But what if this rule is outdated—or even misleading?

In today’s dynamic financial landscape, blindly following the 4% rule could leave you either running out of money too soon or needlessly restricting your spending. Let’s break down why the 4% rule is flawed and explore smarter withdrawal strategies for true financial independence.

The Problem with the 4% Rule

1. It’s Based on Historical Data (That May Not Repeat)

The 4% rule was derived from past market performance, particularly the U.S. stock market’s strong returns in the 20th century. But what if future returns are lower? With rising inflation, geopolitical risks, and unpredictable market cycles, relying solely on history is risky.

2. It Assumes a 30-Year Retirement

Retirees today are living longer. If you retire at 50, a 30-year timeline means your money runs out at 80—but what if you live to 90 or 100? The 4% rule doesn’t account for increasing lifespans.

3. Inflexible Spending Can Hurt You

The rule suggests increasing withdrawals with inflation, even during market crashes. Selling stocks in a downturn locks in losses and reduces future growth potential. A rigid approach can deplete your portfolio faster than expected.

Better Withdrawal Strategies for Financial Independence

1. The Dynamic Withdrawal Strategy

Instead of fixed percentages, adjust withdrawals based on market performance.

-

Good years? Take out more.

-

Bad years? Tighten spending.

This approach helps preserve capital during downturns and maximize gains in bull markets.

2. The Guardrail Strategy (A.K.A. "Floor and Ceiling" Approach)

Set a minimum and maximum withdrawal range (e.g., 3% to 5%).

-

If markets drop, stick to the lower end.

-

If your portfolio grows, allow slightly higher withdrawals.

This keeps spending flexible while protecting your nest egg.

3. Bond Tents for Sequence-of-Returns Risk

Early retirement is vulnerable to sequence risk—poor returns in the first few years can devastate long-term sustainability.

-

Solution: Hold more bonds early on (e.g., 50-60%), then gradually shift to stocks.

-

This reduces volatility when your portfolio is most at risk.

4. The Yield Shield (Living Off Dividends & Interest)

Instead of selling assets, structure your portfolio to generate passive income from:

-

Dividend stocks

-

Bond interest

-

Rental income

This minimizes selling pressure and keeps your principal intact.

5. The "Spend Less, Work Occasionally" Strategy

If markets underperform, consider:

-

Part-time work (consulting, freelancing)

-

Side income (rentals, royalties)

Even small earnings can dramatically reduce withdrawal needs and extend portfolio life.

Final Thoughts: Ditch the Dogma, Stay Flexible

The 4% rule is a starting point, not a law. True financial independence requires adaptability—adjusting withdrawals, diversifying income, and staying vigilant about market conditions.

By using dynamic strategies instead of rigid rules, you can enjoy retirement without the fear of running out of money.

For more insights on smart wealth management, visit Harplight.com.